Demand Has Gone Parabolic. NVIDIA Is Right in the Middle of It.

Q1 2026 Recap | Wiseman Cap

I want you to imagine something simple before we get into any numbers.

Every major country on earth, every large technology company, every hospital system, every bank, and every government agency is trying to build or access artificial intelligence at the same time. Not someday. Right now. And almost all of them need one thing above everything else to make it work. They need the chips and systems that NVIDIA makes.

That is not a metaphor. That is the operating environment NVIDIA just reported into on May 20, 2026. And the numbers that came out of that quarter are some of the most remarkable I have seen from any company in my years of following technology stocks.

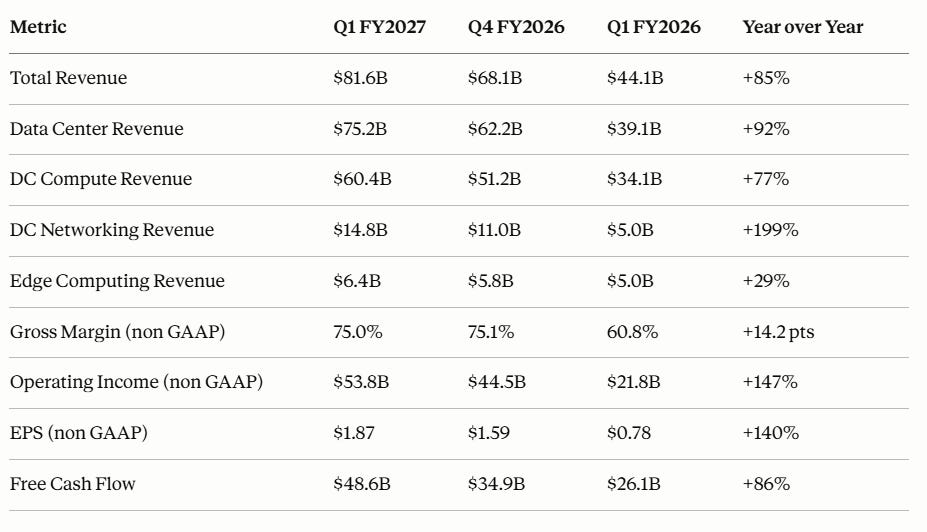

NVIDIA delivered $81.6 billion in revenue for the first quarter of fiscal 2027, up 85% from a year ago and up 20% from the prior quarter. It was the fourteenth straight quarter of sequential revenue growth and the third consecutive quarter where revenue growth accelerated year over year. Most analysts covering the stock now count this as the fifteenth consecutive quarter in which NVIDIA beat Wall Street’s revenue and earnings expectations while raising forward guidance. The $13.5 billion sequential increase in revenue was itself a new company record.

The Numbers

Before the story, here is the scorecard.

Wall Street consensus was expecting $78.9 billion in revenue and $1.77 in earnings per share. NVIDIA delivered $81.6 billion and $1.87. The beat was broad across every segment, with Data Center alone coming in more than $2 billion ahead of consensus expectations.

The number I keep coming back to is buried inside the headline. Data Center revenue grew 92% year over year. In the prior quarter it grew 75%. This business is not slowing down. It is accelerating.

What Is Driving All of This

Before going deeper into the numbers, it helps to understand what is actually powering them.

NVIDIA builds its chips in generations, each one meaningfully more powerful and efficient than the last. The current generation is called Blackwell, and it is the engine behind everything you just read in that table. Every record you see above is Blackwell doing its job across data centers, cloud platforms, and sovereign AI deployments around the world.

The next generation is called Vera Rubin. It combines a brand new GPU architecture with NVIDIA’s first ever purpose built AI CPU called Vera, which the company describes as the world’s first processor designed specifically for agentic AI workloads. Vera Rubin is set to begin shipping later this year, and NVIDIA has already committed to $1 trillion in combined Blackwell and Rubin revenue through 2027. When Jensen Huang talks about an infrastructure buildout unlike anything in history, Blackwell and Vera Rubin are the hardware he is talking about.

Two Stories Inside One Quarter

NVIDIA restructured how it reports its business this quarter, and the new framework tells you a great deal about where management sees the growth going.

Within Data Center, NVIDIA now reports two subsegments. The first is Hyperscale, which covers the large public cloud providers and the biggest consumer internet companies. The second is what NVIDIA calls ACIE, which stands for AI Clouds, Industrial and Enterprise. This covers mid sized AI companies, sovereign governments, manufacturers, and enterprises building their own AI infrastructure.

In Q1, Hyperscale generated $37.9 billion, up 115% year over year and up 12% from the prior quarter. The AI Clouds, Industrial and Enterprise segment generated $37.4 billion, up 74% year over year and up 31% from the prior quarter. Those two numbers are nearly identical in size. That roughly 50/50 split surprised most analysts on the street, who had expected the split to favor hyperscalers at something closer to 60/40 based on commentary from NVIDIA’s GTC conference in March. The balance was better than anticipated and speaks directly to how broadly this buildout is spreading.

The skeptic case on NVIDIA has always been that the company is dangerously dependent on a handful of large technology companies spending massive amounts on data centers. If those companies slow their spending, the argument goes, NVIDIA’s growth falls off a cliff. That argument has much less merit when the enterprise and sovereign segment is running neck and neck with the big cloud players and growing faster sequentially. The diversification of NVIDIA’s customer base is happening faster than most expected, and it changes the risk profile of owning this stock in a meaningful way.

Within the enterprise and sovereign segment, AI cloud revenue more than tripled year over year. Sovereign AI revenue, meaning governments building national AI infrastructure, grew more than 80% year over year and is now deployed across nearly 40 countries. The number of data center sites larger than ten megawatts deploying NVIDIA nearly doubled in a single year, crossing 80 global locations.

Consensus analyst estimates now put full year 2026 hyperscaler capital expenditure at approximately $725 billion, up roughly 73% year over year. That is the ocean NVIDIA is sailing in. And the enterprise and sovereign segment tells us the ocean is wider than the hyperscaler headline suggests.

The Networking Story Nobody Is Talking About

Data Center networking revenue came in at $14.8 billion, up 199% year over year and up 35% from the prior quarter.

Let me say that again plainly. NVIDIA’s networking business nearly tripled in a single year.

This matters because it tells you something important about how customers are buying. They are not just purchasing individual chips. They are buying full systems that include the GPUs, the interconnects, and the networking fabric all together. NVIDIA calls this the AI factory model, and it is the reason the company’s competitive position is more durable than a simple chip comparison would suggest. When a customer builds an AI factory on NVIDIA infrastructure, they are not just buying silicon. They are buying into an integrated stack that would be extremely costly and time consuming to replace.

The InfiniBand networking product line more than quadrupled year over year. A company that was primarily known as a GPU manufacturer now has a networking business that on its own would rank among the most valuable semiconductor revenue lines in the entire industry. Analysts who focus primarily on the GPU numbers are missing a meaningful and rapidly growing piece of the story.

The Vera CPU and Why It Changes the Math

This is the part of the quarter that I believe the market has not fully processed yet.

NVIDIA announced that it has clear line of sight to $20 billion in standalone CPU revenue this fiscal year from its new Vera processor, described by the company as the world’s first processor purpose built for agentic AI workloads. This is a new and entirely separate revenue stream that did not exist a year ago.

The timing is not accidental. Agentic AI systems do not just need GPUs for intensive compute bursts. They need CPUs that can handle context management, orchestration, and the coordination of complex multi step tasks that run over extended periods. NVIDIA built a CPU purpose designed for exactly that workload. Management sees this as opening a $200 billion addressable market for CPU products over time. That figure is notably larger than what AMD had framed the same category at just a few weeks prior.

The Vera Rubin platform, which combines the Vera CPU with NVIDIA’s next generation GPU architecture, is on track to begin shipping in the third quarter of this fiscal year. NVIDIA has reiterated its target of $1 trillion in combined Blackwell and Rubin revenue across 2025 through 2027, and many analysts covering the stock now view that target as conservative given the CPU revenue layer that did not exist when it was originally communicated.

It is also worth noting what NVIDIA said about the performance improvements on its current platform. Management reported a 2.7 times throughput improvement and a 60% reduction in cost per token over the prior six months on Blackwell Ultra. Analysts covering the infrastructure buildout broadly estimate that NVIDIA is driving token cost reductions of more than 70% on an annual basis for its customers. Lower cost per token means more use cases become economically viable, which means more deployments, which means more demand for the underlying infrastructure. It is a reinforcing loop.

The Guidance and What the China Absence Means

NVIDIA guided Q2 revenue to $91 billion, well ahead of the approximately $87 billion consensus Wall Street estimate. That implies another 12% sequential increase and roughly 95% growth year over year, which represents an acceleration even from an already strong Q1.

There is one disclosure buried in that guidance number that every NVIDIA investor should sit with for a moment. NVIDIA is not assuming any Data Center compute revenue from China in the Q2 outlook. No H20 chips, no H200 chips, nothing. The US government has approved export licenses for H200 shipments to China, but China’s own import approval process remains unresolved. NVIDIA left it out of guidance entirely.

The company is guiding to $91 billion without its second largest potential market contributing a single dollar of data center compute revenue. That is an extraordinary statement about the strength of demand everywhere else. If and when the China situation resolves, it represents pure upside to already exceptional numbers. Analysts across the board flag this as optionality rather than risk.

The Financials Beyond Revenue

Free cash flow for the quarter was $48.6 billion. If that pace holds through the year, NVIDIA would be generating cash at a rate approaching $200 billion annually. That is an assumption worth watching, but even a fraction of that number represents extraordinary cash generation by any standard.

Gross margins held at 75.0%, essentially unchanged from the prior quarter and dramatically better than the 60.8% NVIDIA was generating just one year ago. Management guided margins flat at 75% for Q2 and reiterated mid 70s gross margins for the full fiscal year.

One financial trend worth watching carefully is operating expense growth. Operating expenses are expected to grow in the high 40% range for the full fiscal year, up from prior guidance of low 40%. This reflects higher research and development spending and increased use of AI tools inside NVIDIA’s own engineering operations. The company is investing aggressively in its future, which is the right call given the scale of the opportunity, but it does mean some operating leverage is being absorbed by cost growth. Analysts largely view this as appropriate reinvestment rather than a structural concern, but it is something to track each quarter.

NVIDIA ended the quarter with inventory of $25.8 billion and total supply purchase commitments of $119 billion, for a combined $144.8 billion in total supply obligations, up $28 billion from the prior quarter. About $95 billion of those purchase commitments are earmarked for the current fiscal year alone. That number tells you NVIDIA is not managing quarter to quarter. It has locked in supply agreements well in advance because it can already see the demand coming.

Giving Back to Shareholders

NVIDIA returned approximately $20 billion to shareholders in Q1 alone through buybacks and dividends, a company record. On May 18, the board approved an additional $80 billion share repurchase authorization on top of the $38.5 billion already remaining, bringing the total authorization to approximately $118.5 billion.

The dividend increase signals something important about management’s confidence. NVIDIA raised its quarterly dividend from one cent per share to twenty five cents per share, a 25 times increase in a single announcement. That is not a company hedging its bets. That is a management team that believes the current level of cash generation is durable, not cyclical.

Why the Long Term Case Still Holds

I am long NVDA and have been building conviction in this position. The stock trades at a premium to most of the market, and I understand why some investors hesitate at a five trillion dollar market capitalization.

But when I look at the full picture from this quarter, I keep arriving at the same conclusion. We are still in the early to middle stages of a capital spending cycle that has no clear precedent. Enterprise AI deployments are just beginning to scale. Sovereign governments are building national AI infrastructure from scratch. Agentic AI systems, which require dramatically more compute per task than conversational AI, are moving from pilot projects to production deployments across industries. Physical AI, meaning robots, autonomous vehicles, and industrial automation, surpassed $9 billion in trailing twelve month revenue for NVIDIA and is still years from its peak.

Each of these waves needs accelerated compute. Each of them defaults to NVIDIA’s platform because the CUDA software ecosystem, built over more than a decade, creates a switching cost that no competitor has yet overcome. Developers learn on CUDA. Companies build on CUDA. When you train a model on NVIDIA infrastructure, you tend to run inference on NVIDIA infrastructure too.

Analysts tracking the AI infrastructure buildout broadly estimate that for every dollar spent on NVIDIA hardware, there is a multiplier effect of eight to ten dollars across the broader technology ecosystem. That framing helps explain why hyperscaler capital expenditure keeps rising even as each new generation of chips delivers better performance per dollar.

The risks are real and worth stating plainly. Custom silicon from hyperscalers is a genuine competitive consideration over a multi year horizon. Operating expenses growing faster than previously guided is something to monitor each quarter. And China remains an unresolved wildcard that cuts both ways. The law of large numbers is also a genuine challenge. NVIDIA is now one of the largest companies in the world by market capitalization, which creates structural constraints on how much the stock can outperform the index regardless of how well the business performs.

But none of those risks change my view that the underlying business is doing something historically unusual. NVIDIA generated $48.6 billion in free cash flow in a single quarter, is growing revenue at 85% year over year, entering a $200 billion CPU market with purpose built technology, and sitting at the center of what Jensen Huang himself called the largest infrastructure buildout in human history.

On the earnings call, he said demand has gone parabolic. The reason is simple. Agentic AI has arrived.

The numbers this quarter make it hard to argue otherwise.

Disclosure. I am long NVDA. Nothing written here is financial advice. Please do your own research before making any investment decisions.