Shopify - The Quiet Acceleration

How Shopify grew faster this quarter than it did three years ago, and why the platform is just getting started - Q1 2026 Recap | Wiseman Cap

There is something unusual happening at Shopify that I think deserves serious attention from anyone who follows growth technology. The business is getting bigger and growing faster at the same time. Revenue growth went from 27% a year ago to 31%, then 32%, then 31%, and now 34.3% in Q1 2026 on a revenue base approaching thirteen billion dollars annualized. That is not how compounding businesses are supposed to behave at scale. Growth rates are supposed to moderate as the denominator gets larger. Shopify is doing the opposite. As Harley Finkelstein said on the call, Shopify has now put up four straight quarters of 30% or more revenue and GMV growth alongside mid to high teens free cash flow margins every single quarter. I want to walk through what the numbers actually said, what the broker community got right and got wrong in their models, and what I think the market is still underpricing.

The Numbers First

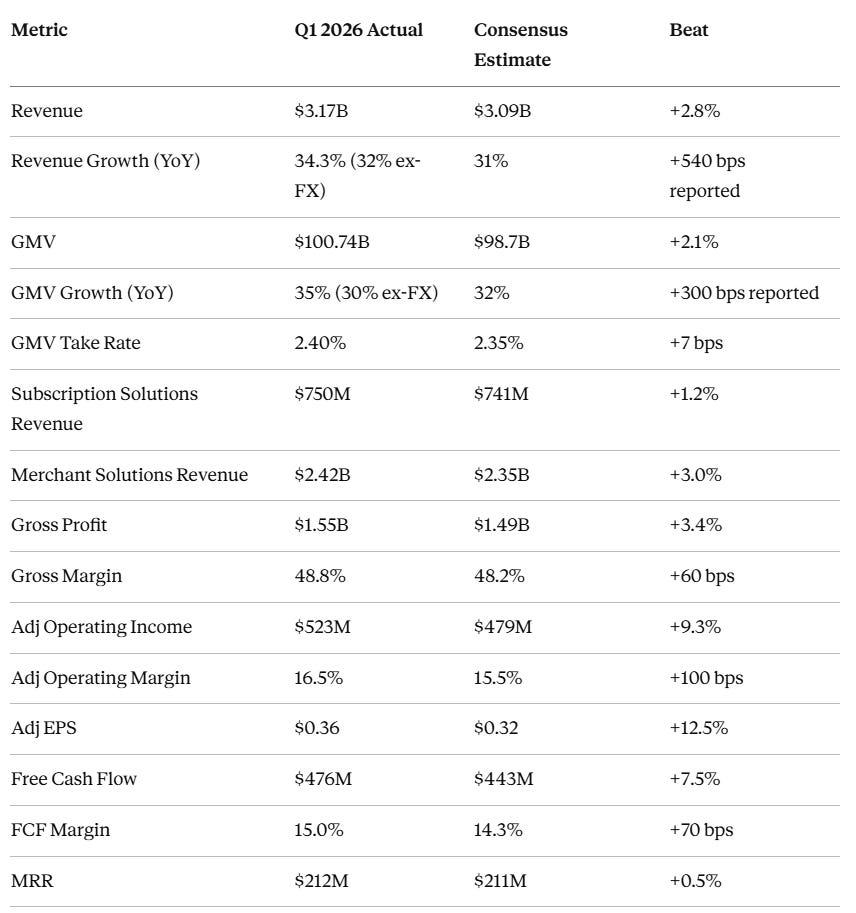

Let me put the Q1 2026 results on the table before anything else, because the gap between what Shopify delivered and what Wall Street expected tells a meaningful part of the story.

Every single line beat. Not one metric missed. Every major consensus estimate across revenue, GMV, gross profit, operating income, EPS, and free cash flow came in ahead of expectations. This was also the eleventh consecutive quarter of 20% or greater GMV growth. The stock fell nine percent the next day. I will explain exactly why that happened and why I think the reaction was wrong.

One thing I want to address upfront before moving into the business narrative. The reported revenue growth of 34.3% and GMV growth of 35% each carried meaningful foreign exchange tailwinds in Q1. Currency effects added approximately five percentage points to GMV growth and two percentage points to revenue growth. On a constant currency basis, GMV grew 30% and revenue grew 32%. Both figures are still strong, and both still beat consensus expectations, but the constant currency context matters enormously for understanding the Q2 guidance reaction, which I will come to shortly.

The GAAP Loss Is Not the Business

The GAAP net loss for Q1 2026 was $581 million, and if you saw that headline without context you would reasonably be concerned. The operating business was solidly profitable. Operating income nearly doubled year over year to $382 million. What drove the GAAP loss was a $1.08 billion non-cash mark-to-market write-down on Shopify’s public equity portfolio, driven primarily by share price declines during the quarter in three holdings: Affirm Holdings at approximately $581 million, Klaviyo at approximately $239 million, and Global-E Online at approximately $186 million. These are paper losses tied to stock price movements in companies Shopify holds as minority stakes but does not operate. Strip them out and adjusted net income for the quarter was $360 million, an increase of $134 million year over year.

The Mix Tells You Everything

Merchant Solutions revenue grew 39.1% in Q1 2026, its highest growth rate in four or more years, outpacing overall revenue growth of 34.3% by five full percentage points. This mix dynamic is not an accident. It reflects deliberate strategy and has meaningful implications for how the business compounds over time.

What drove the outperformance was GMV growth and Shopify Payments penetration expansion. One number worth flagging is that the differential between Merchant Solutions revenue growth and GMV growth narrowed to four percentage points in Q1, down from six points that characterized Q1 through Q3 of 2025. I think there is something to that observation over a long enough horizon, but the Payments acceleration I will detail shortly tells the opposite story in the near term.

Subscription Solutions grew 21%, accelerating from 17% in Q4, with MRR up 16.5% to $212 million. Q1 2026 was the last quarter in which the three-month free trial rollout from Q1 2025 distorted the MRR comparables, so the picture gets cleaner from here. Plus plans account for 35% of total MRR, up from 34% a year ago.

The Cohort Engine Nobody Talks About Enough

The most important statement on the Q1 call was not about AI or enterprise wins. It was about retention. Almost 90% of Q1 revenue came from merchants who have been on the platform for more than a year, and those older cohorts are not plateauing. Each new cohort stacks on top of the prior one, starting at larger initial scale. GMV growth was balanced between same-store sales and new merchant acquisition, which tells you the existing base is genuinely thriving, not just growing through new adds. Merchants in the $2 million to $25 million GMV band added the most incremental revenue, while the $25 million-plus segment grew fastest. The number of merchants doing $100 million or more in annual GMV has nearly doubled over two years, with that segment’s share of total revenue up over 200 basis points in the same period.

It Is Accelerating Everywhere

What made Q1 2026 particularly notable is that growth was broad across geographies, merchant sizes, and channels simultaneously. This combination gives the bull thesis structural resilience that single-vector growth stories do not have.

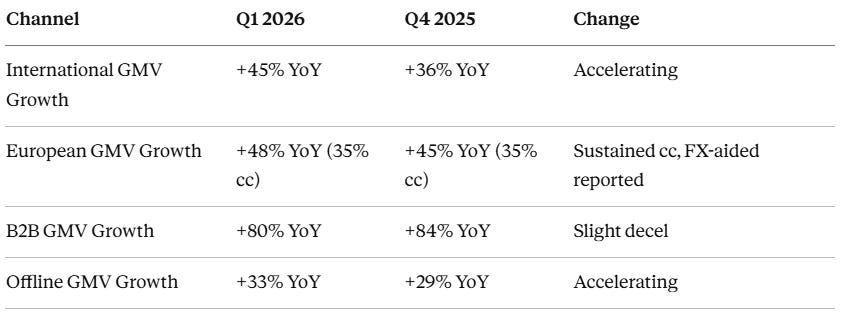

The channels with multi-quarter trending data tell the clearest story first.

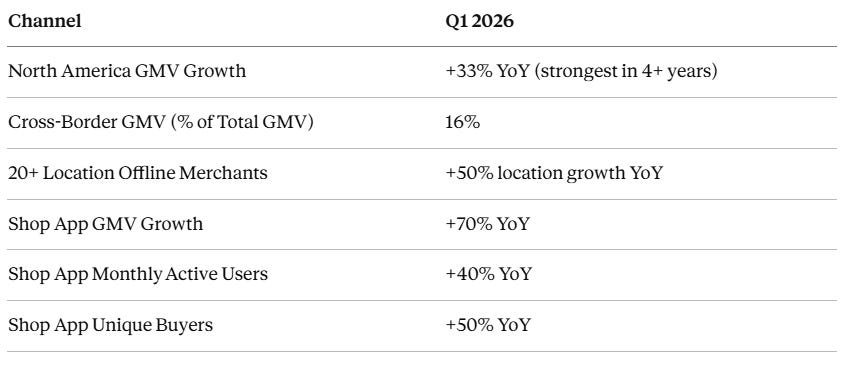

The remaining channel highlights are specific to Q1 2026 but equally important.

Enterprise momentum is broad and the names are getting bigger. In Q1 the platform signed Mulberry, LVMH, Rag and Bone, The Outnet, Lands End, Orvis, and BevMo migrating all of its physical retail locations. The Benetton Group, Victoria’s Secret Body, Epic Shop by Vail Resorts, and Reitmans also went live. Shopify now powers more than 14% of total US e-commerce sales.

The international and B2B numbers in the trending table above tell a clear story. Europe is gaining momentum in constant currency terms even as reported numbers benefit from FX. B2B is decelerating from very high levels but remains one of the fastest-growing segments in commerce infrastructure, and Shopify just expanded B2B tools to standard subscription plans, which broadens the addressable base meaningfully.

Payments Is the Embedded Moat

Every time a merchant processes a transaction through Shopify Payments rather than a third-party processor, the financial relationship between that merchant and Shopify deepens materially. The merchant’s cash conversion cycles, transaction data, customer checkout behavior, and capital access all flow through Shopify’s infrastructure. That is a set of switching costs that does not show up in any single quarter’s reported metrics but accumulates into a durable competitive moat over time.

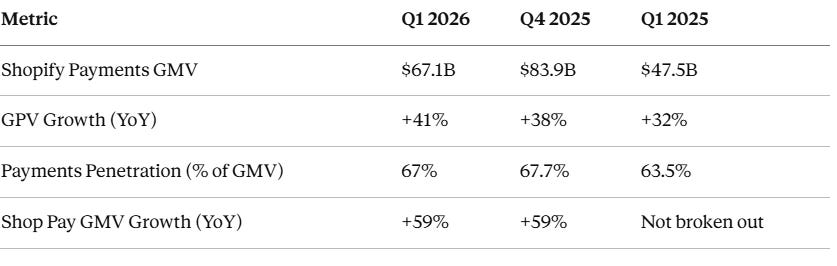

Internationally, Shop Pay GMV grew over 70% year over year in Q1 2026, driven by expansion across 15 European countries and Mexico where Shopify launched payments last year. The penetration trajectory has moved in one direction for years, from 63.5% a year ago to 67.7% in Q4 2025 and 67% in Q1 2026 on a seasonally lighter GMV base. Every point of penetration across a $400 billion annualized GMV base is high-margin incremental revenue.

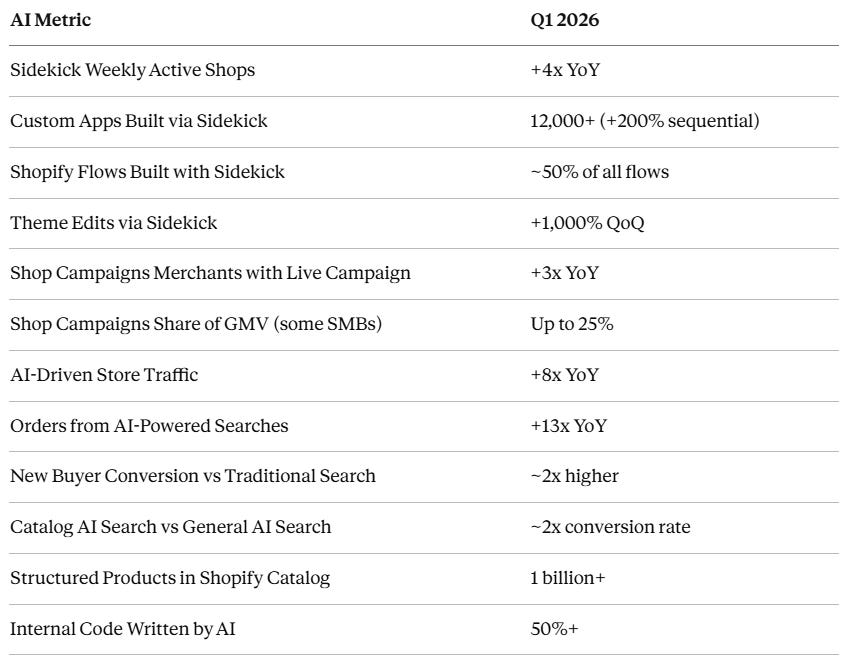

AI Is a Product Reality Here, Not a Label

Harley Finkelstein opened the Q1 call with a line worth anchoring the entire AI discussion to: “AI is now Shopify’s native language.” That is not a marketing statement. The company bet early on AI and forced its adoption internally before the market expected it, and the results are showing up in the metrics.

The catalog stat explains why the conversion advantage is durable. Shopify has structured over one billion products with clean attributes, real-time pricing, and verified inventory. General AI agents searching the broader web work from scraped, outdated data. That information gap is why catalog-powered searches convert at twice the rate, and it is not something a new entrant builds overnight. Shop Campaigns is equally underappreciated: paid discovery has historically been expensive and out of reach for smaller merchants, and the fact that some SMBs are now running up to 25% of their GMV through Campaigns suggests Shopify is becoming a demand creation platform, not just a demand conversion one.

The product dimension getting almost no attention is Pulse, Sidekick’s proactive feature. Where Sidekick responds to requests, Pulse watches the business and surfaces opportunities without being asked. Harley’s example on the call, an accessory brand getting picked up by fashion publications and celebrity Instagram. Pulse detected the buzz, suggested a social proof page, and Sidekick built it in minutes at zero cost. What used to take weeks of marketing and design work is now autonomous. On the cost side, rising AI token costs are compressing Subscription Solutions gross margins modestly, and that pressure will continue as adoption grows. The strategic offset is the Universal Commerce Protocol, an open standard for agentic commerce co-developed with Google, with Amazon, Meta, Microsoft, Salesforce, and Stripe already in the tech council. Shopify is not just using AI. It is positioning itself as the infrastructure layer for it.

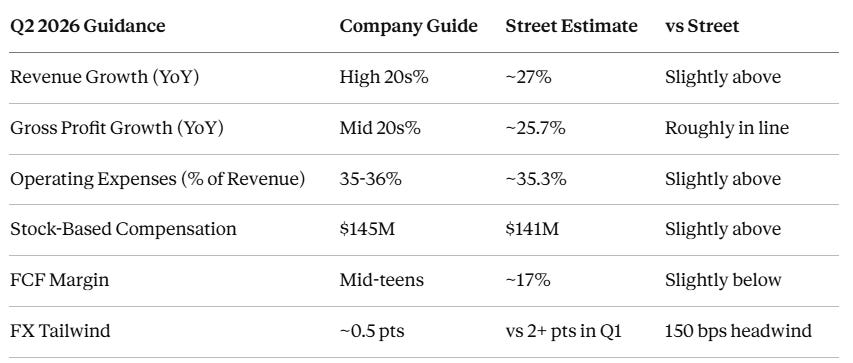

The Guidance Was Not a Warning

Operating expenses came in at 36.7% of revenue, below the company’s own guidance of 37 to 38%, with R&D, S&M, and G&A all declining as a percentage of revenue year over year. Adjusted operating margin of 16.5% beat consensus by 100 to 140 basis points. Shopify also returned $491 million to shareholders through buybacks while producing $476 million in free cash flow in the same quarter.

Gross margin compressed slightly to 48.8% from 49.5% a year ago, a direct consequence of Merchant Solutions growing at 39% while Subscription Solutions grows at 21%. This is an intentional mix shift, not deterioration. Gross profit has grown at a 29% three-year CAGR. A business compounding gross profit dollars at that rate while expanding its payments moat is making a deliberate trade-off that makes complete sense.

The Q2 guidance deceleration from 34.3% to high-twenties looks dramatic but is mostly mechanical. FX tailwinds shrink from two-plus percentage points in Q1 to about half a point in Q2, and Q2 2025 was a tougher 31.1% comp versus Q1 2025’s 26.8%. Strip those out and the constant-currency trajectory is far more consistent than the headline implies. Historically, results have come in around 400 basis points ahead of guidance, which would suggest low-thirties growth in Q2 if that pattern holds.

The Setup From Here

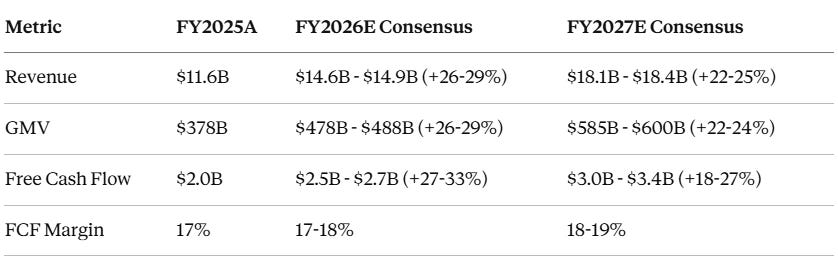

Consensus numbers moved higher across the board following the print, reflecting the GMV acceleration and stronger payments penetration.

These revisions reflect genuine fundamental improvement, not just the headline beat.

What You Are Paying For

Shopify trades at approximately 9 times NTM EV to Sales, down from 14 times at year-end 2025 and 42% below its ten-year average of 15 times, sitting in the second-lowest quartile of its own three-year range of 7 to 17 times. On free cash flow, that is roughly 49 times FY2026 and 38 times FY2027. Fast-growing SaaS peers trade at around 8 times NTM EV to Sales, so Shopify commands a modest premium that looks justified given its take rate economics and payments moat. A business compounding GMV at 30% in constant currency on a $400 billion base looks genuinely appealing at 9 times forward revenue.

The Risks I Am Watching

Three things I am watching. Transaction and loan losses hit $116 million, or 3.7% of revenue, up from 3.2% a year ago, and merchant cash advance receivables grew to $2.10 billion from $1.78 billion at year-end. Shopify Capital is growing fast and the loss rate is still being calibrated on newer products. If the macro deteriorates, this becomes a real drag. Separately, gross profit grew 32% against revenue growth of 34.3%, and management expects that gap to persist in Q2. If it widens, operating leverage may not fully offset it.

The tariff and de minimis picture is worth watching. Channel checks from analysts suggest new merchant additions and migrations softened in Q1, the first visible deceleration since COVID, driven primarily by US businesses. The rebound in Q2 appears underway and global merchants proved more resilient throughout, but this bears monitoring.

Why I Think the Platform Is Just Getting Started

Shopify is simultaneously growing revenue at 34% on a scale that most platforms only dream about, expanding payments penetration quarter by quarter, accelerating into enterprise and B2B markets that are each substantially larger than its core business, building what may become the technical standard for agentic commerce, and achieving operating leverage through AI-driven efficiency. That combination of vectors working in parallel at this scale is genuinely rare.

The cohort dynamics compound in a way that makes the revenue stream more durable than most growth companies at this stage. The UCP bet is asymmetric. If agentic commerce grows into a meaningful share of global commerce and Shopify’s open protocol becomes the infrastructure for it, the monetization opportunity is far larger than the current multiple implies. And if the agentic thesis does not fully materialize, the payments penetration story, the B2B expansion, the Shop App growth, and the international trajectory each independently support the investment case on their own terms.

The quiet acceleration is not quiet to anyone paying close attention, and I think what it implies for the next several years is deeply underappreciated at current prices.

I initiated a starter position in SHOP last week and intend to add on further conviction.

The above represents my personal views and research and does not constitute financial advice. Please conduct your own due diligence before making any investment decisions.

What’s the best metric to value SHOP? With high SBC and 62 x FCF never got the courage to initiate the position. I like the business a lot though.